Table of Content

ARM might be a good option if you can afford the monthly payments, even if they increase. Moreover, it can be a wise choice if a decrease in interest rates is anticipated. According to the amendments made in 2020, VA loan limits are no longer applicable to a person with full entitlement.

Since your credit score isn't taken into consideration when you apply for a VA loan, you are always going to pay a lower interest rate. For traditional mortgages, a person's credit score can have a dramatic - and very negative - impact on the rate that they end up paying. For every 20 points that their credit score dips below 720, traditional borrowers pay a higher rate. Regardless of what your credit score may be, you'll enjoy the same interest rates that someone with impeccable credit would enjoy when you qualify for a VA home loan. Enter your ZIP code and the calculator will take your county's VA loan limits into consideration to let you know if a down payment is required. There are a variety of factors that play into the calculation of your monthly loan payment.

VA Mortgage Limits

If you are using Internet Explorer, you may need to select to 'Allow Blocked Content' to view this calculator. Talk with a loan officer if you may have problems fulfilling the occupancy requirement. That $426,200 figure represents how much you could look to borrow before factoring in a down payment.

In the case of a mortgage, you would have to pay the premium as part of your monthly installments. A fixed-rate mortgage is a home loan with a rate of interest that remains constant throughout the life of the loan. If your home costs more than the defined VA limits, you have three options. This means that the VA will either pay 25% of the loan amount or $36,000 to the lenders if the borrower defaults in any way. While getting your COE is the starting point of getting a VA home loan, it is not the only step. You must also satisfy the lender’s requirements and ensure that the property meets all the MPRs.

Home Sale Calculator

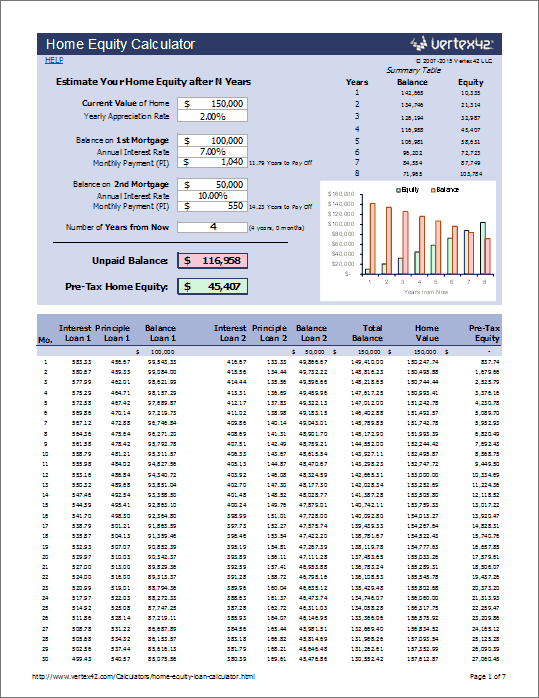

Use our amortization calculator to estimate your monthly principal and interest payments made over the life of a loan. Making prepayments can potentially shorten the loan term and reduce the interest payments. In the More Options input section of the calculator is an Extra Payments section to input monthly, yearly, or single payments. Use the results to see how much can be saved by making extra payments in terms of interest paid as well as the reduction in loan term.

Typically, the factors affecting your monthly payment include the home price, down payment, interest rate, and if you have to pay the VA funding fee. An amortization schedule for a VA loan is a breakdown of your monthly VA mortgage payments over the life of the loan. Amortization tables typically break down the principal and interest paid over time. The funding fee is a governmental fee paid to the Department of Veterans Affairs to help keep the VA loan program running for years to come. The VA funding fee ranges from .5 to 3.6 percent and not every borrower is required to pay it.

VA Loan After VA Foreclosure

The fifth section of the calculator contains multiple important variables for veterans. Namely it lists VA status, loan use & if the funding fee is financed in the loan. By default these are set to active duty/retired military, first time use & funding fee financed. The original VA loan would need to be paid in full to pursue the one-time restoration. You can’t take advantage of this if you’re still making mortgage payments on the property. It’s important to understand that lenders typically treat this as an “offset” and not as effective income.

The VA has eliminated county loan limits effective January 1, 2020. Previously, VA homebuyers were limited to the corresponding county conforming loan limit when purchasing a home with 100% financing. When a home's purchase price exceeded the county loan limit in the past, a VA homebuyer would have been required to make a down payment. VA home loans also carry lower credit score requirements than many conventional loan programs and don’t require borrowers to make a down payment or pay mortgage insurance premiums.

With this type of home loan, the VA agrees to pay your lender 25% of the loan amount in the event you default on the mortgage. Your VA loan entitlement plays a major role in determining what size mortgage you can get without making a down payment. Every eligible service member has a basic entitlement of $36,000 for loans up to $144,000. There are also secondary — or second-tier — entitlements that vary depending on your county. Veterans and military members purchasing in more expensive housing markets typically have more VA loan entitlement.

Those with reduced entitlement -- either because of one or more active VA loans or default on a previous VA loan -- may have to factor in a down payment when the time comes. Department of Veterans Affairs to provide eligible homeowners and buyers the help needed to buy, build, repair or refinance a home as long as it's a primary residence. These include brokerage fees, real estate commissions, and title insurance. A VA approved lender; Not endorsed or sponsored by the Dept. of Veterans Affairs or any government agency.

When those two are fully in place, Veterans can borrow as much as a lender is willing to lend without the need for a down payment. Bankrate is compensated in exchange for featured placement of sponsored products and services, or your clicking on links posted on this website. This compensation may impact how, where and in what order products appear. Bankrate.com does not include all companies or all available products. It’s possible for you to lose your VA loan entitlement permanently.

In order to qualify, the property must fit within the specific criteria as outlined by the VA. Although it's not terribly common, occasionally the VA requires repairs and other work to be performed before it will approve a loan. The seller is not allowed to make the repairs; it is solely the responsibility of the buyer.

We’re transparent about how we are able to bring quality content, competitive rates, and useful tools to you by explaining how we make money. Our experts have been helping you master your money for over four decades. We continually strive to provide consumers with the expert advice and tools needed to succeed throughout life’s financial journey.

No comments:

Post a Comment